Personal Finance Equations

The equations of personal finance are a bit complicated because they involve so many variables and conditions. Unless you are dealing with 'simple interest' (we're not in this app) the equations are based on the idea of 'exponential growth' and that alone makes them somewhat nasty.

All equations in this app have been field-tested with the TVM app featured in the TI-Graphing Calculator family.

Numworks also features an online financial calculator in the 'Solver' area! Check it out! (When using this calculator, money going out of your pocket is negative; money coming into your pocket is positive.)

The 4 financial apps are based on the intimidating equations below. The following tables show the primary variables involved followed by intermediate variables to simplify the complexity of the equations.

| Concept | Equation | Comment(s) |

|---|---|---|

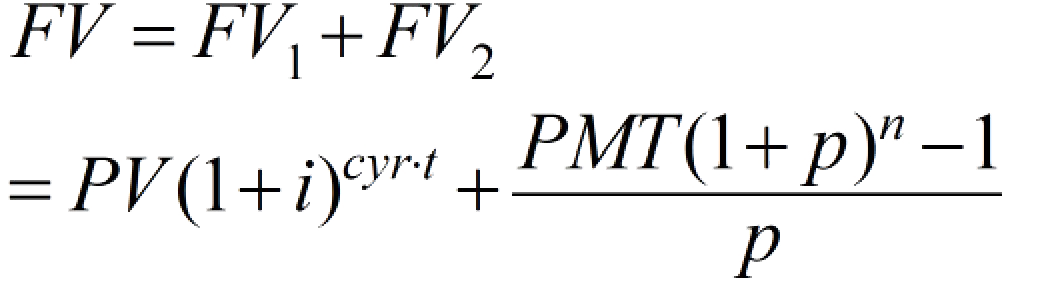

Savings Savings |

|

FV1 contributes value due to the compounding of the principal (present) value. FV2 contributes value due to the compounding of the regular payments |

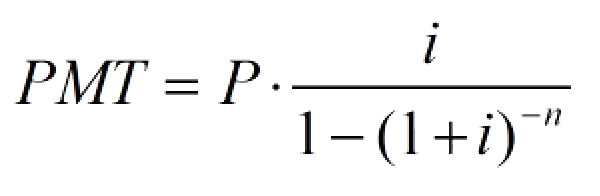

Loan Loan |

|

Currently, our app assumes both monthly payments and compounding |

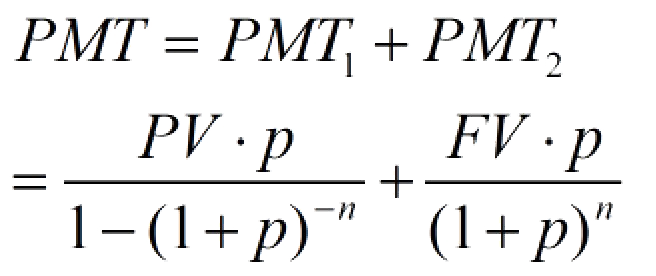

Sinking Fund Sinking Fund |

|

PMT1 contributes value based on the PV (principal value), while PMT2 contributes value based on the FV |

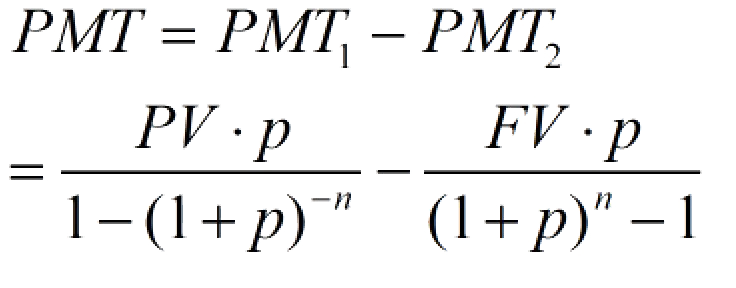

Annuity Annuity |

|

PMT1 contributes value based on the PV (principal value), while PMT2 contributes value based on the FV. Pro tip: When using this app, if you let the Future Value equal the Principal, the money will never 'drain' and the PMT will be 'perpetual!' The reason PMT2 is subtracted is because if FV > 0, that means some money will still be left in the account at the end of the time period. Therefore, that money does not contribute to the overall regular payments received during the term of the annuity. |

| Concept | Symbol | Comment(s) |

|---|---|---|

| Principal | P | The 'lump sum' amount invested or saved. In our app, this is often synonymous with PV. See below |

| Present Value | PV | In our apps, this variable may be synonymous with Principal, P. According to Investopedia: Present value (PV) is the current value of a future sum of money or stream of cash flows given a specified rate of return |

| Annual Percentage Rate (APR) | r | Annual rate of interest expressed as a decimal. Interest is the either the fee a financial agency charges for the use of their money, or the dividend it pays you for the use of your money |

| Investment time in years | t | The length of time that an investment or loan is 'in play' |

| Regular periodic payment | PMT | Regular payments made to reduce debt or to increase the value of an investment |

| Payments per year | pyr | The frequency with which payments are made. This value is often 12 (monthly) but can also be, commonly, 1 (annually) or 4 (quarterly) |

| Compounding per year | cyr | The frequency with which an agency pays or charges interest. This value is often 1 (annually), 4 (quarterly) or 12 (monthly) |

| Future Value | FV | The amount of money (return or debt) expected in the future as a result of the interplay between P, r, t and PMT |

To make the Personal Finance Equations a bit easier to program, there are some intermediate variables that were created to ease the complexity. This was especially important for situations where p/y and c/y were not the same values.

| Symbol | Comment(s) |

|---|---|

| i | APR/Compounding per year: r/cyrIn the source code, you will see this referred to as myI |

| c | Compounding per year/Payments per year: cyr/pyrIn the source code, you will see this referred to as littleC |

| p | (1 + i)c - 1This variable uses i and c as defined above. In the source code, you may see this referred to as littleP |

| n | t·pyrRepresents the total number of payments made in the time interval |